Prefect competition is a market in which there are many firms selling identical products with no firm large enough, relative to the entire market, to be able to influence market price

Perfect Competition-Assumptions

There are a large number of firms in the industry.

The firms are usually small in size and with small market shares.

Due to their small outputs they cannot affect the whole industry output and thus are ‘price takers’.

All firms produce identical or homogeneous products

There are no barriers to entry or exit.

Producers and consumers have perfect knowledge of the market i.e. prices and products.

There is prefect resource mobility i.e. all the resources can be switched/allocated in the most profitable manner.

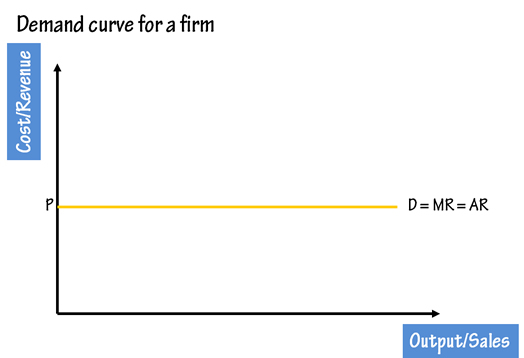

Perfect Competition-Revenue Curve

The right hand part of the diagram looks at the demand for an individual firm which is tiny relative to the whole market. It cannot influence price. It faces a horizontal demand ‘curve’ at £5. Average revenue is constant at £5. The firm’s AR curve must lie along exactly the same line as the demand curve. (the firm’s demand curve). Marginal Revenue will be the same as average revenue in this case. Selling one more unit at a constant price adds the amount to total revenue.

|

Price |

Quantity |

TR (P X Q) |

AR (TR/Q) |

MR |

|

$5 |

1 |

$5 |

$5 |

$5 |

|

$5 |

2 |

$10 |

$5 |

$5 |

|

$5 |

3 |

$15 |

$5 |

$5 |

|

$5 |

4 |

$20 |

$5 |

$5 |

As price is constant, total revenue will rise at a constant rate as more is sold. TR curve is a straight line through the origin. When a firm is a price taker its AR & MR curves are a horizontal line at the given price.

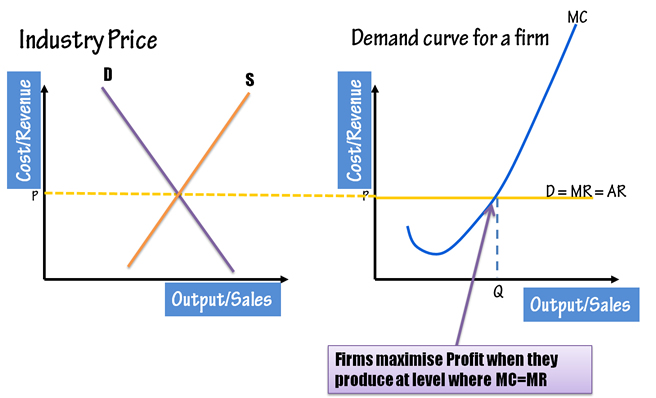

In prefect competition, the industry will face normal demand and supply curve i.e. demand curve slopes downwards and supply curve is upward sloping. The reason being suppliers are willing to supply more at higher prices and consumers are willing to buy more at lower prices. Thus the price in the industry is the equilibrium point.

In prefect competition, a firm is price taker, thus it has to adopt the prevalent price in the industry.

The reason being, if they increase their price then the consumer will switch to another firm as the all the firms produce homogenous products and moreover, consumers have perfect knowledge of producers who can supply goods at lower prices.

The demand curve for a firm in perfect competition is perfectly elastic because a firm can sell any quantity at the industry price.

The diagram given below, illustrates that a firm in perfect competition derives its price from the industry price.

Due to the fact that a firm does not have to reduce its price in order to sell more, its MR= AR which is equal to P or D

Profit Maximisation

Profit maximisation level of output for a firm is where MC=MR

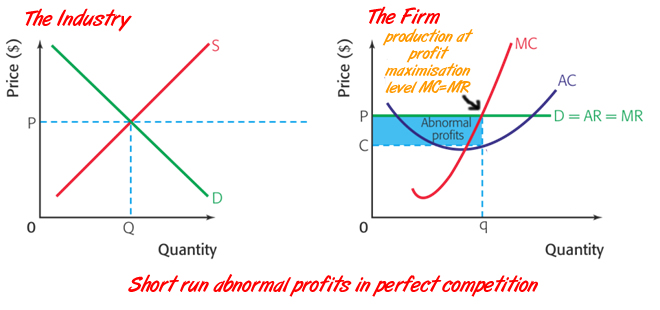

Short run profit in Perfect competition

In the short run, a firm in perfect competition can make abnormal profits. It may be due to some cost advantages due to technological changes or some production innovation. This means the firm will be covering more than the economic cost (total cost + opportunity cost)

The diagram below illustrates that firm is producing at Q which is the profit maximisation level of output (MC=MR).

At this output the firms Average Cost (AC) is at C and its Average Revenue is at P, thus leading to abnormal profit for the firm P-C. (Shaded blue region)

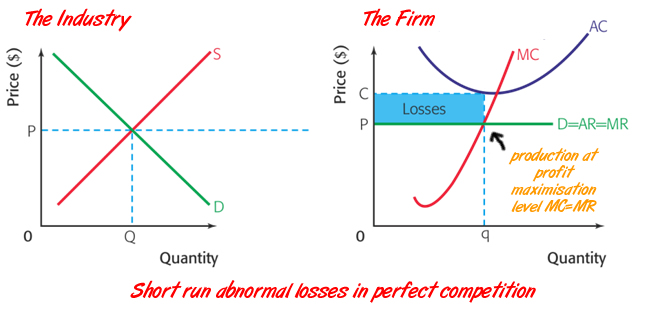

Short run losses in Perfect competition

There may be cases, when a firm may not be able to cover its Total cost due to some inefficiency in their production process. As the diagram below show the firm is producing at Profit Maximisation level of output (MC=MR), its AC is C which is more than its AR (at P), thus leading to a loss C-P (Shaded in blue).

Profit maximization in the long run

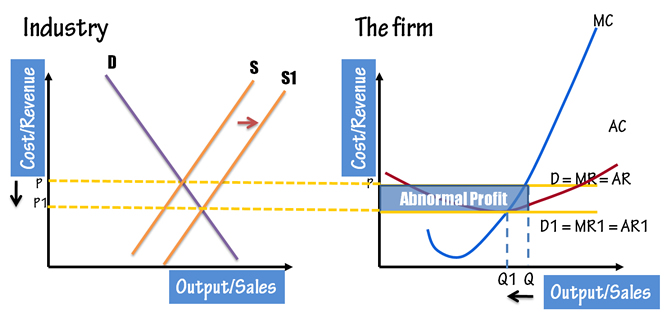

Moving from short run abnormal profit to long run normal profit

As we know that there are no barriers to entry in a perfectly competitive market, the moment a firm starts making abnormal profits, more firms will be attracted by that and will start entering the industry. This will lead to an increase in supply, which will lead to a fall in industry prices.

The firm is a price taker and thus prices for it will also fall and the demand curve will shift downwards.

And in the long run its abnormal profits will vanish and the firm will have normal profits only.

As we can see in the diagram above, the industry price is P and the firm takes its price from the industry price. The firm is making abnormal profits by producing at q (Profit Maximisation level) and is having an abnormal profit P-C.

Now look at the industry graph, more firms are attracted, which results in a increase in supply (shift of supply curve from S to S1). This leads to a lower in the industry price to P1. The firm has to take this price P1 and its demand curve shifts downwards i.e. D1=AR1=MR1

At this point the existing firms will not leave the industry as they can cover their economic cost and new firms will stop entering the industry as there is no more abnormal profits. The industry has reached long term equilibrium.

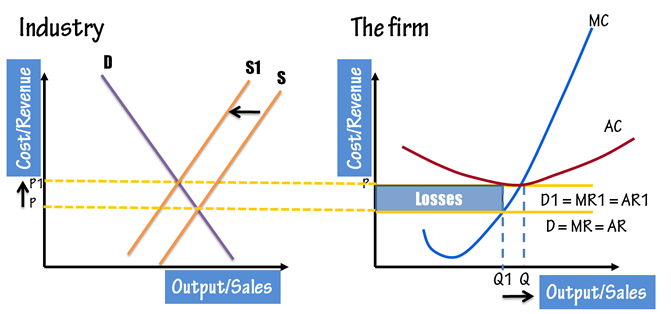

Moving from short run abnormal profit to long run normal profit

In the short run a firms in a perfectly competitive market might make losses. In this case the firms will start shut down as there is no sunk cost. The supply in the industry will go down pushing the prices up and the firms will start making normal profits in the long run.

Looking at the firm diagram below, we see the firm producing at profit maximising level q is making a loss (C-P)as its AC is above the AR. However, as more and more firms start leaving the industry the industry supply curve shifts to the left to S1. This raises the price in the industry. Due to the fact that the firm is a ‘price taker’ it will lead to the upward movement of firm’s demand curve from D to D1 resulting in reduction of losses. The process will continue firms in the industry are making losses.

The industry has reached its long term equilibrium where no more firms will enter or exit the industry and all the firms will be making normal profits

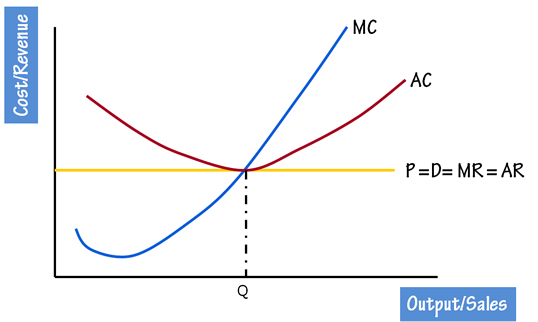

Long Run

In the long run a firm in a perfectly competitive market will be make normal profits.

The firms produce at q which is the profit maximising level of output.

Firms make normal profit as AC is equal to AR

Advantages of perfect competition

- P = MC; Production is at minimum AC; only normal profits will be made in the long run. No supernormal profits, so consumers gain from low prices.

- If consumer’s tastes change, the resulting price change will lead firms to respond. An increase in consumer demand will call forth-extra supply.

- Perfect competition is said to lead to consumer sovereignty. Consumers through the market determine what and how much is to be produced. Firms cannot manipulate the market.

- They cannot control price. The only thing they can do to increase profit is to become more efficient, which also benefits the consumer. If a firm is efficient it will earn supernormal profits (in the short run).

- Competition between firms acts as a spur to efficiency. There is no point in advertising as all the products are the same.

- The desire for supernormal profits and the desire to avoid a loss will encourage the development of new technology.

Disadvantages of perfect competition

- Firms may not be able to afford research and development. Investment may be considered a waste of money, as one’s rivals will copy new production techniques. The product is homogeneous.

- The lack of variety is a disadvantage to the consumer. Under monopolistic competition and oligopoly there is often intense competition over the quality and design of the product. This can lead to pressure on firms to improve their products. This doesn’t exist in perfect competition. There is therefore a lack of competition over product design and specification.